Q3 2020

U.S. Economic Insight:

A pivotal tug of war

While widespread vaccinations should accelerate growth, the economy could face other challenges

A pivotal tug of war

While the general population sees the world through the lens of the pandemic (writ large), we take a broader approach when analyzing the economy in 2020. We view the economy through the lens of uncertainty. In economics, we define uncertainty as the element we cannot quantify because of inadequate data or information. That contrasts with risk, which we can quantify with adequate data and information. Of course, the pandemic significantly contributes to the massive uncertainty that we are confronting, but uncertainty for the economy involves many components and dimensions, not just the pandemic. As we have attempted to peer through the fog of this uncertainty in 2020, we have acknowledged this challenge.

“…the economy will gain momentum as we move through and ultimately past the pandemic.”

As we approach the end of this year, we thankfully have greater transparency than at any previous point since the outbreak began. Although much uncertainty remains, it has lessened to the point where the shape of the outlook is coming into view. Yet that brings both good news and bad news for the economy. Ultimately, this tug of war between good news and bad news will determine the path of the economy over the very short run, where the uncertainty lies. We remain confident in our short-run and medium-run outlooks: the economy will gain momentum as we move through and ultimately past the pandemic. But much can go wrong between now and then. Ultimately, this confines the greatest remaining uncertainty to a narrow period of time that will remain critical to the path forward for the economy and the commercial real estate (CRE) market.

The good news

On one side of the divide stands the good news. A few key developments drive the good news for this outlook. First, the election occurred. That matters for two reasons. The results themselves provide transparency on policy, which helps to eliminate uncertainty. Uncertainty remains a paralyzing force because it causes people (and by extension, organizations) to delay making decisions until uncertainty abates because they do not want to make mistakes. Even if an undesired outcome occurs, the certainty enables better decision-making. Additionally, while control of the Senate will remain undecided until early January, probability suggests that divided government will persist with the incoming administration. Under such an environment, marginal, not transformative, policy making seems most likely, providing a measure of stability to businesses and markets.

“After the worst quarterly growth rate in U.S. economic history during the second quarter, the third quarter produced the best quarterly growth rate in history.”

Second, the recovery thus far has outperformed relative to expectations from earlier this year. That does not downplay the severity of what occurred but highlights the relatively strong snap back thus far. After the worst quarterly growth rate in U.S. economic history during the second quarter, the third quarter produced the best quarterly growth rate in history. Some of this occurred simply by dint of mathematics: growth rebounded from a low base and merely reopening some of the economy produced positive growth. But federal government stimulus played an important role in the U.S. economy outperforming many expectations as well as outperforming most other major economies of the world. Even though the economy cannot and is not sustaining this breakneck pace, the rebound places GDP closer to its pre-pandemic apex than its nadir during the second quarter of 2020.

Relative outperformance of the U.S. economy

Third, the positive news on the development of effective vaccines does not alter our timeline for when vaccines move us past the pandemic. But the effectiveness of the vaccines, well above expectations, bodes well for economic recovery. The high rates of effectiveness (above 90%) should not only immunize members of the population, enabling them to reengage the economy, but should also reduce transmission, bringing case levels down so that even the non-immunized can more safely participate in economic activities. Empirical evidence demonstrates that all else equal, lower case levels translates into stronger economic activity.

The bad news

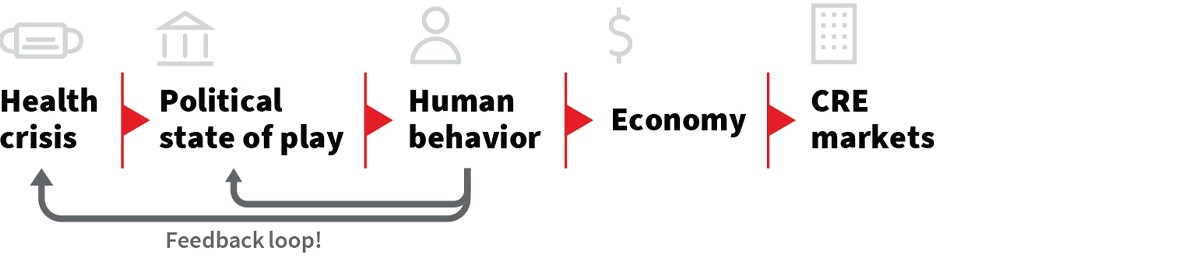

On the other side of the divide stands the bad news. First, the pandemic itself is escalating once again. This sits in line with our base case forecast: we projected an increase in cases to new record-highs with the return of colder weather to the Northern Hemisphere coupled with the fact that we never truly brought the pandemic under control. But we acknowledge that the trajectory could exceed the assumptions embedded in our base case outlook. That could occur if we get caught in a feedback loop whereby our behaviors worsen the pandemic and consequently affect the political state of play, causing more severe government edicts (that aim to slow the pandemic) than we are assuming in our base case. Last week’s Thanksgiving holiday and associated travel, as well as the remainder of the upcoming holiday season, could accelerate the growth rate above our base expectations. How does this impact the economic outlook? On the supply side of the economy, a worsening pandemic increases the use of measures that slow the spread of the outbreak (e.g. curfews, shutdowns, lockdowns, limited business capacity). But the measures prove detrimental to economic growth in the very short run by restricting the ability of business to generate goods and services. On the demand side of the economy, as the outbreak worsens, fear of falling ill dissuades many people from engaging in economic activities that potentially put their health at risk such as shopping, dining, and traveling.

Pandemic's impact on the economy

Second, we remain concerned about the gradually expiring fiscal support that undoubtedly helped the economy rebound as strongly as it did. Since July, the expiration of different support structures has tugged against the recovery. Without renewal, remaining support measures will expire by the end of this year. Even controlling for the inevitable slowdown in the recovery from third quarter’s pace, the lack of fiscal support is restraining growth. Across a variety of metrics and sectors of the economy, the slowing in economic activity shows clearly. Maybe the best example of this is the savings rate. With robust fiscal support, many households ably saved some of their support funds for a future rainy day. But the savings rate continues to decline as these measures expire and many households increasingly resort to spending out of savings to fund expenses. We estimate that households will exhaust the marginal increase in savings by the end of this year.

Third, the recent announcement that the Treasury will allow the expiration of a number of the Federal Reserve’s (Fed’s) emergency lending facilities while withdrawing roughly $454 billion of funds that the Fed could lend if needed. Although the Fed is not actively lending via these facilities, the markets viewed them as an important safety net option that the government could utilize if necessary. That does not take away all of the Fed’s firepower, but severely limits it. The Fed still retains the ability to lend, if necessary, at a lower level and the Fed could continue to expand its balance sheet via asset purchases. In fact, all else equal, the expiration of these lending facilities increases the probability that the Fed will further expand its balance sheet to support the economy.

Ready, Set, Go!

We retain a positive growth outlook for the holiday season and the fourth quarter. Higher-income households, which represent the majority of consumption in the U.S., have largely recovered from the crisis. Higher-wage, higher-skill jobs have essentially regained all of the jobs lost earlier in the year. With asset markets continuing to reach record-high levels, affluent consumers should also benefit from the wealth effect, whereby households consume more as their wealth increases. Meanwhile, fiscal stimulus measures, though diminished, remain in place, helping to support less-affluent households. And households can dip into their diminished savings to help fuel their holiday spending.

“Although the pandemic will not disappear like flipping a switch… widespread vaccinations should enable growth to accelerate.”

Which side wins this tug of war? Our base case scenario projects modest growth in the first half of 2021, but risks to the downside are building and our downside case scenario continues to show a second (though more modest) contraction in GDP. We are operating under the (necessary) assumption that vaccination begins this month and continues thereafter, vaccinating most of the population by mid-2021. Although the pandemic will not disappear like flipping a switch at that point, widespread vaccinations should enable growth to accelerate . Our base case scenario also assumes a modest fiscal stimulus package of roughly $1 trillion that does not impact the economy until the first quarter of 2021. Both Democrats and Republicans continue to agree on more support and a worsening health crisis could force them to come to an agreement out of necessity. In this scenario, the good wins the tug of war. And If Congress passes a larger fiscal stimulus package than we are assuming or the vaccine distribution occurs faster than we anticipate, then the trajectory of the economy could outperform our base case and head toward our upside case.

But, if the pandemic accelerates beyond our underlying assumption (which is already rather dire) or no fiscal stimulus package passes Congress, then the economy could head toward our downside case scenario. Under this scenario, economic growth contracts once again during the first half of 2021. While we project that any such contraction would pale by comparison to the significant contraction in GDP during the first half of 2020, it would nonetheless produce a larger hole for the economy to climb out of during the post-pandemic recovery. We still believe the good news ultimately wins the tug of war by mid-2021, but in this scenario the bad news makes the contest much more difficult and painful over the next few quarters.

| Pulling for CRE |

For CRE, our scenario-based forecast shows overall challenging times ahead in 2021 as would be expected in this part of the cycle, irrespective of how the tug of war plays out. While the cycles of the different property types do not synchronize perfectly, CRE generally lags the overall economy and the downturn in the CRE market typically lasts longer than the downturn in the economy. Retail and hotel properties have seen a significant impact and will likely take some time to stabilize. For office markets where many tenants are in “wait and see” mode, activity remains subdued, concessions have already increased and our proprietary modeling indicates that asking rents will continue to decline as vacancy increases further in 2021. We expect this recovery to be somewhat bifurcated, with the best-quality, well-located assets and markets with favorable demand and demographic flows experiencing less decline and quicker recovery, while older or “commodity” assets with weaker locations or rent rolls will likely struggle. Industrial and multihousing remain active and are poised to weather the downturn relatively well, while some specialty sectors like life sciences and data centers have been running “hot” even through the pandemic. For capital markets, transaction volumes have already fallen quickly and impacted pricing and liquidity, especially for sectors with weaker fundamentals and uncertain outlook. Year-over-year transaction volume during the third quarter increased from the bottom, offering some hope for stabilization as investors start to look toward a recovery. In addition, low interest rates are driving allocations to the sector and shifting some strategies to opportunistic offense.

| Closing thoughts |

Developments over the last quarter have improved transparency and provided hope for the economy as we head into 2021. A rebound in economic growth, followed by the conclusion of the presidential election, and better-than-expected news on vaccines firms up our short-run and medium-run outlooks. Economics provides us with no guarantees, but we have greater clarity now than at any point in time in the last nine months.

For now, the remaining uncertainty predominantly rests in the tug of war over the very short run (roughly the next six months). If 2020 has taught us anything, we should expect the unexpected. The roll out of the vaccine over the next few months could present downside risks, particularly if states that are already suffering from budget shortfalls lack appropriate funding needing to distribute and administer vaccines. Only once people become vaccinated will the situation begin to improve. Fiscal stimulus could certainly help, but passage of another package remains a dicey proposition. And even if a package were passed, support for state and municipal governments might get excluded. The run-off elections for Georgia’s Senate seats could also surprise, handing control to the Democrats, but that seems improbable. And then pandemic could unfold in several ways. While forecasts currently point to a significant worsening over the next couple of months, that could also serve to alter behaviors, potentially a mitigating force.