Healthcare delivery strategies pivot in a COVID-19 environment

A new report from JLL outlines how real estate is supporting emerging patient and clinician preferences.

CHICAGO, Jul. 14, 2020 – COVID-19 has accelerated trends for delivery of healthcare and changed the contours of the patient-provider relationship. The new Healthcare Real Estate Outlook from JLL outlines three key concepts for healthcare real estate occupiers and investors to keep in mind to maximize their efficiency and productivity.

Trend #1: Advances in telehealth will reinforce rather than replace on-site care.

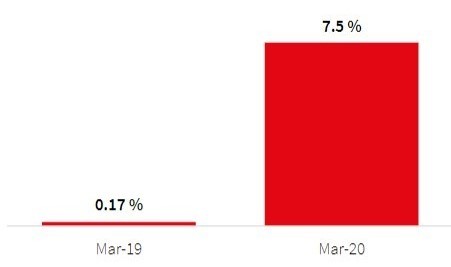

COVID-19 and the ensuing CARES Act dramatically expanded telehealth reach, lifting restrictions on where and how patients can access virtual care. According to FAIR Health’s private insurance claims data, during the first quarter of 2019, only 0.17 percent of all services were provided via telehealth. In March 2020, that usage jumped to about 7.5 percent, with April and May levels, not yet available, forecasted to be higher. Total telehealth visits are estimated to approach 1 billion for 2020, an exponential increase from 2019’s minimal base level.

Telehealth services: 2019 vs. 2020

As medical technology continues to rapidly advance, an increasingly sophisticated suite of wearables and robotic telemedicine carts will enhance home monitoring and management, allowing telehealth to provide increased points of access to healthcare. This rising tide of demand will comprise on-site services as well, as more frequent systematic touchpoints will produce more live-care follow-up appointments.

“COVID has shifted the paradigm, but the idea of telehealth replacing in-person, on-site care is probably overstated,” said Jay Johnson, National Director, JLL Healthcare Markets. “Telehealth will displace some on-site care, but it will also expand access to treatment that might not have otherwise occurred, and much of that will involve a live-care component with a visit to a healthcare facility. The focus should be on adapting real estate to new modes of care delivery.”

Trend #2: COVID-19 will accelerate segmentation of wellness and acute care in real estate.

The pandemic has increased the need for higher-acuity space within hospitals and accentuated the existing migration of lower-acuity space into alternative locations. An increase is expected in facilities that emphasize wellness, prevention and a healthy lifestyle, all of which feature lower acuity and lower system-wide costs. These facilities will likely emerge via grouped primary and specialty care and will locate as near as possible to the consumer to maximize convenience. And, with both destination and neighborhood shopping center availability and affordability on the rise, healthcare tenants are increasingly locating within retail properties to benefit from foot traffic and accessibility.

“Future success for hospitals means embracing this shift to higher-acuity care to also appease consumer concern about safety within hospital facilities,” said Richard Taylor, Divisional President, JLL Healthcare Solutions. “Better segmentation of patients and ability to control facilities, whether a permanent or temporary as-needed configuration, will be key to minimizing disruption of services during future pandemics or crises.”

Trend #3: Medical office facilities and investment to benefit in a post-COVID-19 environment.

Occupancy within the 1.5 billion square feet of medical office space across the United States has fluctuated within a remarkably narrow band—between 91 percent and 93 percent—between the Great Financial Crisis and today. The medical office investment thesis is strong and sound, offering long-term leases, stable occupancy and income, strong tenant credit quality, and tenant retention to keep investor eyes keen.

“While many clinical operations were reduced or shuttered during COVID-19, tenants continued to pay rent,” said Audrey Symes, Research Director, JLL Healthcare and Life Sciences. “Rent collections by the largest owners of medical office space were consistently noted in the high 90 percent range throughout the lockdown period, with limited rent deferment and relief required. This performance illustrates both the cyclical and structural tailwinds enjoyed by medical office investments.”

As a result of the growing investor interest, typical sales volumes per year have more than doubled, from $6.8 billion in 2012 to $14.7 billion by 2017. Since 2017, sales volume has remained above $13 billion, illustrating the staying power as a true real estate investment sector.

“Two-thirds of medical office square footage is owned by health systems and physicians with strong access to capital,” said Mindy Berman, Managing Director, JLL Healthcare Capital Markets. “Large investment opportunities are likely to present themselves as COVID-19 steepens the differentiation in health system resources.”

JLL Healthcare enhances the patient experience, improves clinical outcomes, and drives financial performance through real estate and facilities solutions. The group provides dedicated support to manage real estate needs, facilities, guidance on portfolio optimization and location strategy, financing support for purchase or development, and assists systems and investors throughout the healthcare spectrum. For more news, videos, and research resources on JLL Healthcare, please visit the firm’s healthcare web page.

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. JLL shapes the future of real estate for a better world by using the most advanced technology to create rewarding opportunities, amazing spaces and sustainable real estate solutions for our clients, our people and our communities. JLL is a Fortune 500 company with annual revenue of $18.0 billion, operations in over 80 countries and a global workforce of more than 94,000 as of March 31, 2020. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.com.