Walkability: why it is important to your CRE property value

With mounting evidence of a strong correlation between walkability and commercial real estate economics, the walkability trend is here to stay

Walkable areas are some of the most desired urban locations for residents and employees seeking convenience, unique experiences and access to amenities, making them highly desirable to commercial real estate investors.

What Does Walkability Mean for Commercial Real Estate

Research shows that improved walkability, including proximity to public transit, has a positive effect on a host of commercial real estate metrics. An improvement in Walk Score®, the yardstick by which many measure how walkable a particular address, neighborhood and city are, strongly correlates with an increase in property values, rents, retail sales, occupancy, absorption and price resilience in downturns.

According to a study conducted by HR&A and commissioned by NoMa Business Improvement District in Washington, D.C., mixed-use developments outperform single-use properties in both CBD and suburban settings alike. Similarly, mixed-use projects located in suburban areas tend to outperform their single-use suburban peers. Shifting preferences among both the millennial and baby boomer generations, which are each gravitating toward new urban environments, drive the outperformance of these walkable developments. The outperformance can also be explained by companies that leverage walkability and strong amenities to attract top-tier talent and are willing to pay a rent premium for highly-walkable space. What is perhaps most salient to property investors is that there is still a great lack of “highly-walkable” real estate supply across property types in the U.S. This may represent a significant generational investment opportunity.

Increased Walkability = Higher Property Values and Rents

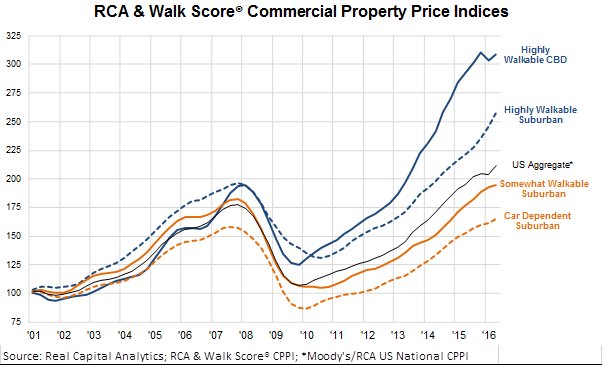

There is a direct correlation between increased walkability and price appreciation. Last year, Real Capital Analytics and Walk Score launched the RCA & Walk Score Commercial Property Price Indices (CPPI). According to their analysis, prices for properties located in CBDs have risen 125 percent over the past decade, while comparable properties located in car-dependent areas have risen only around 20 percent during the same time period. Additionally, properties don’t have to be located in purely urban areas to benefit; the index finds that prices for suburban properties that are also considered highly walkable are up 43 percent.

Mariela Alfonso, in writing for the Urban Land Institute, estimates that a 10-point increase in Walk Score is associated with an increase of five to eight percent in commercial values. Where a public transit station is located close to a subject property, the Brookings Institution has observed that this causes a 40 to 200 percent price premium, and ULI also pins this figure at “more than 40 percent.” A similar trend applies to multi-housing and single-family residential. ULI has found that a one-point increase in Walk Score translates to home price premiums ranging from $700 to $3,000 per unit. Brookings Institution and State of Place™, an urban data analytics platform that measures the aspects of the built environment that affect walkability, found in a study of 162 U.S. urban areas that, for each level of increase in the five-level State of Place Index, “office rents rose nearly $9 per square foot, retail rents increased $7 per square foot, residential rents rose $300 per unit and for-sale residential values climbed more than $81 per square foot."

The impact walkability has on rent growth is significant. Earlier this year, George Washington’s Center for Real Estate and Urban Analysis published a study by Christopher Leinberger and Michael Rodriguez that specifically looked at how economic performance relates to rental rate premiums in commercial property types, noting that:

“There are substantial and growing rental rate premiums for walkable urban office (90 percent), retail (71 percent) and rental multi-family (66 percent) over drivable suburban products. Combined, these three product types have a 74 percent rental premium over drivable suburban. Walkable urban market share growth in office and multi-family rental has increased in all 30 of the largest metros between 2010 and 2015.”

Increased Foot Traffic Also Leads to Increased Retail Sales

Studies have shown that if an opportunity for greater density and improved walkability is created then this strategic foresight will attract higher levels of foot traffic and retail sales. A New York City Department of Transportation study found that the addition of a series of pedestrian and bicycle infrastructure projects located adjacent to a studied property increased retail sales there 49 percent compared to three percent borough-wide. Additionally, “small expansions of pedestrian rights-of-way were tied to a 49 percent reduction in commercial vacancies” and “a conversion of a curb lane into outdoor seating increas[ed] pedestrian numbers by more than 75 percent and increased sales at bordering businesses by 14 percent.” Additionally, the previously mentioned Brookings Institute study found that “retail sales rose 80 percent" for each level increase in the five-level State of Place Index.

Opportunity for Creating More Walkable Real Estate

The average Walk Score in the U.S. is only a 48 out of 100, which would be described as “car-dependent,” the second-lowest Walk Score category. Given that such a strong relationship exists between user preference for more walkable real estate and rising property values, one might believe that more Americans would wish to access this type of built environment and that commercial real estate values would respond accordingly. A well-executed investment strategy with a focus toward walkability, combined with sound real estate market fundamentals, may prove compelling for the right investor and for the right urban opportunity.