Opportunity Zones: the commercial real estate topic du jour

A summary of Opportunity Zone basics, regulation updates, outstanding questions, issues and some of the business opportunities across various markets country wide

It is tough to have a conversation about commercial real estate today without discussing Opportunity Zone investing. Opportunity funds can provide extraordinary tax benefits by investing in Opportunity Zones, but there are a lot of nuances that need to be appreciated. This article will summarize the basics; cover some of the updates from the October 19, 2018, OZ regulations update; present some of the outstanding questions and issues; as well as discuss some of the business opportunities we are seeing in various markets across the country.

In December 2017, Congress passed the Tax Cuts and Jobs Act, and, through it, the Opportunity Zones Program was created. It allows investors to roll capital gains tax liabilities into new investments on a tax-deferred basis and, with certain conditions met, enjoy a waiver of capital gains tax on appreciation from such investment. With U.S. investors currently holding approximately $6.1 trillion in unrealized capital gains, the source for this capital is plentiful.

Qualified opportunity funds make investments in communities that have been certified as Opportunity Zones. Taxpayers then become eligible to receive significant tax benefits in three ways:

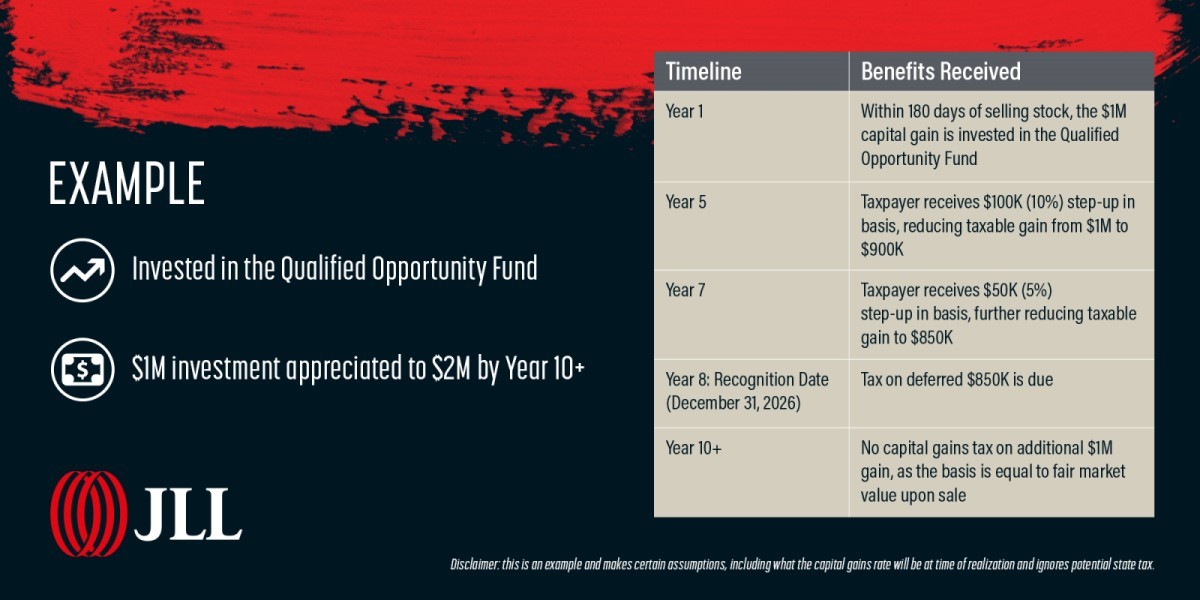

1. Capital Gains Deferral

- The taxpayer has 180 days in which to reinvest capital gains into a qualified opportunity fund

- Reinvesting capital gains allows tax payers to defer capital gains tax until the “recognition date,” which is the earlier of disposition, or December 31, 2026.

- At the recognition date, the taxpayer must pay capital gains tax on the initial investment at the short- or long-term capital gains rate depending on the types of gains originally invested.

2. Step-Up in Basis of the Original Investment

- At the time of investment in the fund, the deferred gain basis begins at zero.

- After five years, the basis increases to 10%.

- After seven years, the basis increases to 15%

3. Capital Gains Exclusion

If a taxpayer holds the investment in the Qualified Opportunity Fund for at least 10 years and meets the original use or substantial improvement qualification, then the taxpayer will not pay capital gains tax on the appreciation of the investment.

It is important to consider how the Opportunity Zones were selected. that Opportunity Zones were selected from census tracts identified as low-income, nominated by each state governor and designated by the secretary of the treasury. The motivation of each state’s governor was to drive as much Opportunity Zone investment to their state as possible and as such many zones are focused on areas that are already development targets. The last U.S. Census was in 2010, and a lot has changed in some markets since then, so many OZs are overlaid with sub-markets where development is already extremely desirable and have undergone significant gentrification.

A Qualified Opportunity Fund is a vehicle that invests in a Qualified Opportunity Zone business located in an Opportunity Zone. A QOF must be funded by proceeds from a sale that generated either short- or long-term capital gains within 180 days in order to utilize OZ tax benefits. It is important that 90% of assets held by QOFs be QOZ property and fund must have been acquired after December 31, 2017. Qualified Opportunity Funds can include other tax benefit programs including New Market Tax Credits, Low-Income Housing Tax Credit (LIHTC) and Historic Tax Credits.

To be a QOZ business property, its original use must begin in the Opportunity Zone or the Opportunity Fund must substantially improve the property.

- The original use definition is still being finalized but applies mostly to ground up development

- If the original use test is not met the property must be substantially improved, meaning during any 30-month period after acquisition, additions to the basis of the property must exceed the cost basis at acquisition (calculated on buildings net of land)

An interesting comparison in tax benefits is to compare Opportunity Zone investments to a 1031 tax deferred exchange. It allows indefinite deferral of capital gains, while OZ investment requires a recognition of those gains in December of 2026. An OZ investment does not need to be like-kind, can be real or personal property, can only consist of the gains on the sale rather than the entire proceeds from the sale and can be utilized with any short- or long-term capital gains (even those from partnership interests).

The Treasury Department and Internal Revenue Service issued proposed regulations on October 19, 2018, providing much anticipated guidance for OZ investors. The proposed regulations represent significant progress and clarify many ambiguities but leave some aspects needing clarification, which will hopefully be provided with the updates expected later this year. A few of the key takeaways from the October guidance are:

- Any long-term or short-term capital gains that otherwise would be recognized before January 1, 2027, are eligible for deferral.

- In order to realize the capital gains exclusion for an asset held over 10 years, one must sell the asset prior to December 31, 2047. This is 20 years beyond the December 31, 2028, expiration of Opportunity Zones and allows investors a flexible timeline to dispose of an asset.

- A taxpayer that has completely disposed of an Opportunity Fund investment before December 31, 2026, can reinvest the deferred gain into another and make a new deferral election with respect to such gain.

- For purposes of the substantial-improvement requirement (doubling of cost basis) the basis attributable to land is not considered. Establishing the cost basis as just the building net of land better facilitates major rehabilitations and repurposing vacant buildings rather than just development.

While the October regulations significantly improve the clarity for investors, there are still some outstanding questions. The main one is how debt may be restricted. The updated regulations make it clear that borrowing will not impede an investor’s potential Opportunity Fund benefits at acquisition or for development. The risks and issues associated with making leveraged distributions especially prior to realization of the deferred capital gains tax are unclear. This is an important issue as the nature of the investment is likely long term, and there will be a liquidity need to pay deferred capital gains tax at the end of 2026, which would ideally come from property level debt.

With 8,761 designated Opportunity Zones, there are some that stick out as interesting opportunities from a macro perspective and others where the zones represent particularly interesting investment opportunities in specific sub-markets. One such macro opportunity is student housing since OZs were chosen based on low-income communities and many college towns qualified because of their large populations of incomeless students. A similar phenomenon applies in many resort destinations, where incomes are often low despite opportunities for development. In studying the Opportunity Zone map, many qualified areas are in booming areas that have already enjoyed significant development and employment growth. Some particularly interesting geographies include San Jose, Oakland, Portland, Los Angeles, Chicago, Boston, New York, Texas and many more that have already experienced significant gentrification and development demand.

Opportunity Zone investment represents one of the most exciting opportunities of our commercial real estate generation. The October guidance gives investors' confidence to move forward in structuring and putting together deals while awaiting final clarity on a few issues. Opportunity Zone investment will not alone justify investment or development, but the tax incentives provided will serve as a tailwind in markets otherwise attractive for investment and development. To date, there have been billions of dollars raised in Opportunity Zone Funds, and JLL is actively marketing and discussing OZ deals for and with clients.