2022 in retrospect

Retail RE fundamentals show solid performance as US recovers from worst effects of pandemic

- Keisha Virtue

As we usher in a new year, it’s often a good exercise to look back at the previous year and reflect on how it’s shaped us. In doing so, we can more accurately predict where we’re heading in the next 12 months and, more importantly, how we can pivot to accomplish even more in the future. In reviewing retail’s performance in 2022, I was struck by how resilient retail has been; despite significant headwinds posed by inflation and rising interest rates, retail performance, on a whole, was rock solid. Here are some highlights from 2022 and a peek at what we can expect in this new year.

Retail net absorption was the highest in five years

2022 was a banner year for retail real estate performance coming out of the pandemic. Retail tenants absorbed nearly 76 million square feet of space during the year – the highest level since 2017. In comparison, 2019 (before the pandemic even hit) saw total net absorption of roughly 38 million; so, 2022 net absorption is twice what it was right before COVID decimated retail performance in 2020. In conjunction with higher demand for space, deliveries have remained low. At 25.4 million, retail space delivered was merely one-third of net retail space taken, which helped push down vacancy levels to a very low 4.2%. During the year, we saw several retail categories aggressively push to expand their footprint. Discounters, home improvement and home goods retailers have been taking medium and large retail spaces. The demand for smaller spaces is being driven primarily by QSRs, mobile retailers and local service providers. Experiential retailers (like Urban Air Adventure and Planet Fitness) are also accelerating new openings, accounting for 15% of leasing activity in 2022 (up from an average of 8-10% annually). Performance isn’t uniform across the board, however. Neighborhood centers and general retail are dominating demand. Malls – with the exception of Class A or lifestyle centers – saw uneven performance during the year.

2022 net absorption highest since 2017

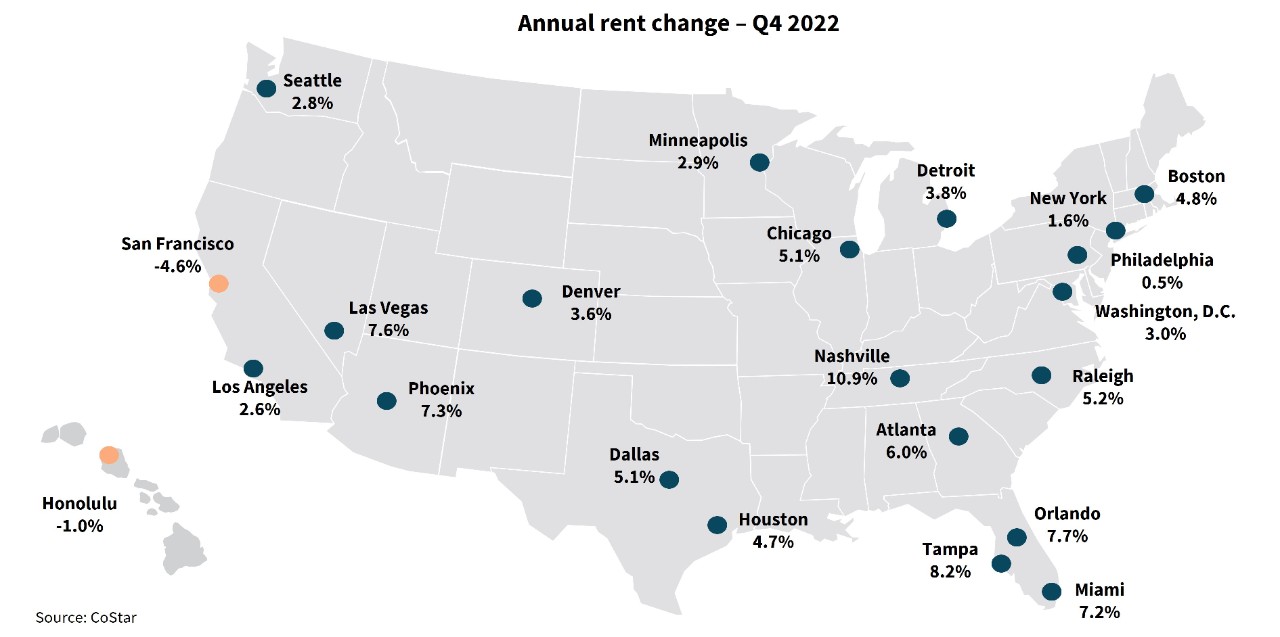

Sun Belt markets maintained the highest annual rent growth

Performance has varied across markets as well. Sun Belt markets in Florida and Texas as well as Phoenix, Las Vegas and Nashville have experienced outstanding rent growth in the last year. While year-over-year rent growth has climbed in northern markers, they still remain comparatively lower than those in the South. San Francisco rents continue to struggle, declining 4.6% from Q4 2021 to Q4 2022.

Most metros see year-over-year rent growth in Q4 2022

Inflation curbed consumer spending

In reviewing the economic climate of 2022, many of us would agree the buzz word has been “inflation”, which soared to a 40-year record annual growth of 9.1% in June. Despite dampening somewhat to 7.1% near the close of the year, inflation had a profound impact on consumer sentiment, shopping behavior and bottom-line sales. Climbing food and gas costs bifurcated consumer spending, causing most consumers to focus on necessities and away from discretionary goods during the year. And, while we did see a 7.6% jump in holiday sales, the numbers are much tamer when accounting for elevated prices.

Soaring inflation dampens consumer spending

Experiential foot traffic saw a renaissance

In 2022, consumers rushed to “return to normal” after staying close to home during the height of the pandemic. Traffic to experiential tenants like theaters, fitness centers and entertainment venues (like Dave & Busters) saw meaningful increases during the year. Furthermore, during December, as consumers celebrated the holidays, traffic to restaurants jumped 11% from the previous month and visits to entertainment attractions more than doubled from November.

During 2022, we saw move-ins from entertainment tenants such as golf attractions, escape rooms, arcades and kids activities (trampoline parks, etc). Given consumers’ continued focus on experience, we can expect to see increased activities from these tenants this year.

Experiential foot traffic rose 28.7% from 2021 to 2022

Retailers will experiment with smaller footprints in 2023

As we surmise about what this new year will bring, one trend that seems likely to gain traction is that of retailers experimenting with the right store size and format. In most cases, that means smaller, more efficient stores. In Q4 2022, the average size of new leases dipped to 3,185 square feet, as store size continued to trend downwards. Retailers will experiment with smaller footprints in 2023

Average new lease size in Q4 dips 3.0% year-over-year

In 2022, we saw a continuation of smaller department store concepts like Bloomies and Market by Macy’s. We have also seen an acceleration of shop-in-shop concepts like Toys “R” Us in Macy’s, Ulta in Target, and Petco in Lowe’s. Best Buy also debuted a smaller digital-first format last year. Given rising costs, many retailers will look to make every square inch of store space count. There are exceptions to this trend, however. Some retailers like Target and H-E-B are doubling down on larger store formats as a bid towards amplifying the shopper experience and allow space for omnichannel fulfillment.

You may also like

Big questions real estate is asking in 2025

Prospects are improving but the real estate industry has much to consider

From wet to dry: How AI is shaking up laboratory design

Changing research methods are altering the DNA of life sciences real estate

Black Friday sees online sales increase by 10%

Black Friday online sales totaled $10.8 billion, with ‘buy now, pay later’ expected to score big this holiday season.