Warning: Changes ahead

Will expiring unemployment benefits help boost the labor market or put a drag on consumer spending and economic growth?

- Ryan Severino

Looking for more insights? Never miss an update.

The latest news, insights and opportunities from global commercial real estate markets straight to your inbox.

Quick takes:

- Changes ahead for the economy

- Tapering announcement coming?

- Inflation slowdown continues?

- Expiring unemployment benefits: good or bad?

- CRE set to take all changes in stride

Information revealed last week, coupled with upcoming events this week, signals likely changes ahead in the economic landscape. Some changes will certainly occur, some changes seem probable, but as the end of summer nears the economic landscape appears set to shift. While the changes should not prove drastic, the combination of a few key, marginal differences could produce some noteworthy outcomes.

“…it appears that the Fed believes that relatively soon the economy should evolve to the point where the Fed feels tapering should commence.”

The first potential change comes via the Fed. At last week’s annual meeting of central bankers in Jackson Hole, Fed Chair Powell managed expectations that the Fed could announce the tapering of asset purchases as soon as November, with the reduction in purchases beginning in likely December or January. Most everyone expected that tapering would occur before changes to interest rate policy, the only real question was about timing. Though they left the door open for the timing of tapering to shift depending upon the economic trajectory over the next few months, it appears that the Fed believes that relatively soon the economy should evolve to the point where the Fed feels tapering should commence. Asset purchases prove most effective when financial markets face severe disruptions, such as last March during the onset of the pandemic. Over time, their impact seems to diminish or at least become ambiguous. With financial markets operating smoothly since last spring and with low interest rates still remaining in place, the downside risk to tapering over the next four to five months appears limited.

More evidence of inflation peaking?

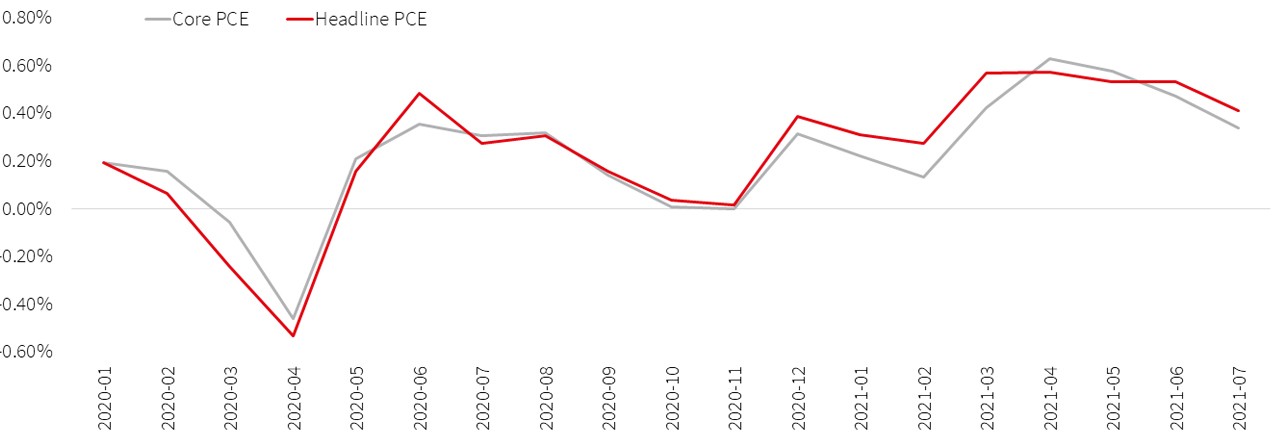

Monthly inflation slowing

Last week also provided more evidence that inflation was peaking, or at least that the rate of increase was slowing. The headline personal consumption expenditures (PCE) index for July increased by 4.2% on a year-over-year basis, accelerating slightly versus the pace from June. But the month-over-month change continued to slow. The monthly change peaked in April and has decelerated for three consecutive months. The core PCE index showed something very similar – the year-over-year change increased very slightly while the month-over-month change also decreased for three consecutive months after peaking in April. This slowing trend should persist as higher prices (base effects) make sustaining high rates of inflation more challenging over time. These patterns largely mirror what we observed in the consumer price index (CPI) data. In short, the data from both major consumer-oriented inflation indexes show that inflation is likely peaking during the summer and should slow in the coming months, much as we anticipated. We continue to caution that it will take time for this slowdown to occur and that inflation should ultimately settle into a range greater than that from the previous business cycle.

“…inflation is likely peaking during the summer and should slow in the coming months, much as we anticipated.”

Will expiring unemployment benefits help or hurt?

The other noteworthy change will come this week, with the expiration of the emergency unemployment benefits. And the implications of that remain uncertain. On the one hand, the expiration of the benefits could incentivize some who have sat on the sidelines of the labor market to return, helping to boost the economy at a time when the labor shortage remains pronounced. On the other hand, the expiration of the benefits could remove income from some consumers and produce a drag on consumer spending and economic growth. The data over the next few months should demonstrate which side holds the stronger argument, but either way it will change the dynamic of the economy as we head into colder months.

| What we are watching this week |

Consumer confidence for August looks set to decline as concerns over inflation and the Delta variant weigh on consumers’ spirits. Both the ISM manufacturing and services indexes for August should continue to show expansion among both sectors of the economy. The August employment situation should show additional strong net job gains, well into the hundreds of thousands, though likely slower than the torrid pace of the last two months. The unemployment rate likely held steady while wages continue to increase amidst the ongoing labor shortage.

“… (CRE) transaction volume appears roughly on par with that from 2019 and pricing looks increasingly robust.”

| What it means for CRE |

The shifting economic landscape should not present major issues for a broadly strengthening commercial real estate (CRE) market. Through mid-year, transaction volume appears roughly on par with that from 2019 and pricing looks increasingly robust. With momentum building behind improving fundamentals across numerous property types, volume and pricing do not appear at risk from tapering. While we have consistently trumpeted the inflation-hedging power of CRE, we do not foresee slowing inflation as a risk to investor appetite. Even as inflation slows, the investors most concerned with it will likely retain their views on both inflation’s future trajectory and CRE’s ability to hedge inflation. Lastly, the removal of unemployment benefits remains a bit of a wild card, but the underlying economic momentum should persist, even as growth slows, providing continued support for both CRE fundamentals and capital markets.

| Thought of the week |

Nominal back-to-school spending is anticipated to set a record this year amidst a return to in-person schooling and somewhat higher prices.

You may also like

The data strikes back

Banks have tightened standards and pulled back on lending activity. Will this quiet banking issues?

Fed Flinches?

Concerns over bank failures led to a softer response from Feds. But how will tightened credit conditions weigh on the economy?

Move fast and break things

A host of banking issues is complicating matters for the Fed, but are there silver linings for commercial real estate?