Five trends demand a new approach to healthcare facilities and real estate

JLL identifies opportunity for CRE and FM partnership to support the journey to population health

CHICAGO, June 20, 2018 — As the healthcare industry shifts toward value-based population health, mergers and acquisitions (M&A) continue to accelerate, creating mega-sized, nontraditional health systems. Meanwhile, the industry continues to grapple with regulatory uncertainty and increasing costs per patient. On the cusp of yet another major transformation, the healthcare industry requires innovative approaches to real estate and facilities.

Whether providers' real estate portfolios and facilities are well-positioned for this change remains a big question mark, according to JLL Healthcare.

"Hospitals are sitting on an enormous amount of underutilized real estate following the intense M&A activity over the past several years, but most organizations still haven't prioritized strategic real estate portfolio planning," said Richard Taylor, Managing Director of JLL Healthcare Solutions. "In an environment of continued transformation and uncertainty, healthcare organizations are leaving money on the table by not optimizing their facilities management and real estate portfolios. We expect more healthcare organizations to tap experienced corporate real estate (CRE) facilities and consultancy partners to fill this strategic gap."

Five healthcare trends to watch

Major trends are transforming how healthcare organizations deliver—and are reimbursed for—patient care, driving new approaches to real estate and facilities. JLL has identified how hospitals and health systems can stay ahead of these five disruptors shaping the healthcare industry:

1) Unprecedented M&A activity is creating mega health systems, cross-industry collaborations and new approaches to CRE. Hospital consolidation has steadily increased in recent years, and that trend continued in 2017. Many 2017 deals are set to close this year, pending federal and state regulatory review. These mergers, as well as never-before-seen cross-industry collaborations with pharmaceutical companies, faith-based organizations and nontraditional healthcare players, will continue to impact the healthcare industry this year. Further, many large healthcare systems are creating their own insurance companies to combat the reduction of reimbursements from large insurance companies.

Consolidation is creating some of the largest systems in the country, along with new kinds of healthcare organizations involving healthcare providers, payers, retailers, pharmaceutical and device companies and other players.

While 2017 may have been the year of hospital M&A, 2018 is likely to surpass last year's deal volumes as hospitals and health systems prepare for value-based reimbursement and the convergence of healthcare providers and retailers.

2) Traditional hospital networks may soon be obsolete, as the definition of a health system evolves. As health systems prepare for the future, payers, faith-based providers and academic institutions merge, while regional consolidation continues.

What does this mean for real estate? Expect fewer big hospitals; greater use of ambulatory surgery buildings; and more emergency clinics and micro-hospitals in local communities. The concept is to engage the population before residents develop acute illnesses that require expensive treatment and manage their care through community facilities rather than a large, centralized facility. More diverse facilities also improve the patient experience and are healthy for the hospital balance sheet, so demand for remote care locations is growing quickly. Outpatient centers often are less expensive to construct and operate than traditional hospitals.

As of year-end 2017, a full 70 percent of medical office building (MOB) construction projects were in off-campus locations, according to JLL's 2018 Healthcare Real Estate Outlook. This is creating a new challenge for healthcare systems that are used to running large campus-based facilities. Managing dispersed portfolios brings new challenges and increased pressures of building or buying real estate services.

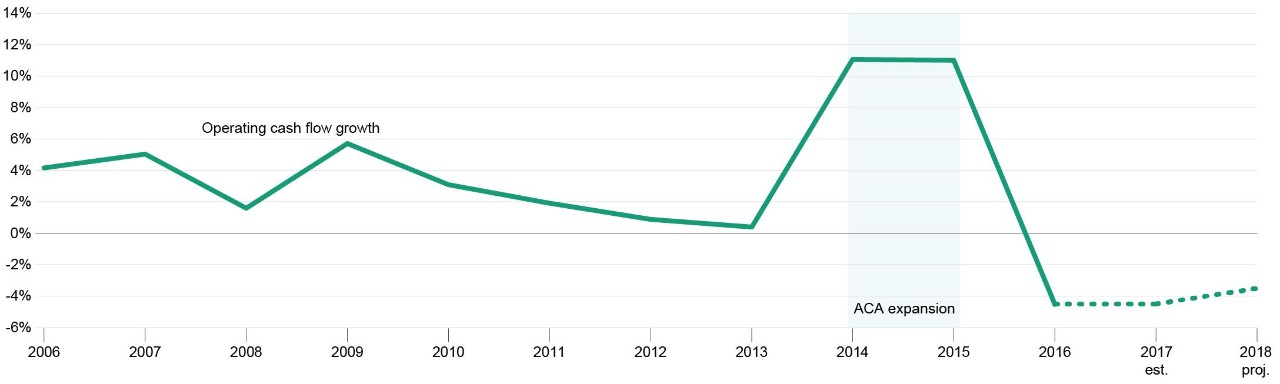

3) Cost-per-patient continues to increase, and operating margins tighten. While specifics around the Affordable Care Act (ACA) may change, hospitals' focus on value-based care will continue as pressure to reduce costs and improve outcomes remains a priority. Regardless of the debate over public policy, the transition to value-based care is already well underway.

"Pressure to reduce costs will continue to increase regardless of what happens with the ACA, and every opportunity to reduce fixed and operating costs should be considered," said Chris Wadley, Senior Vice President and Houston Healthcare and Life Science Lead, JLL. "The acceleration of cost reduction is necessary as costs rise, margins fall, and uninsured populations increase, following the repeal of the individual mandate."

Projections for contracting operating

4) Predictable uncertainty surrounds the reimbursement model. Hospitals traded lower reimbursements for more stability and consistency made possible by insuring a larger portion of the population through the ACA. Now that the individual mandate has been repealed as a part of the Tax Cuts and Jobs Act, care providers will reabsorb financial risk, leaving considerable uncertainty.

Concurrently, while providing a high-quality patient care experience has always been a top ethical priority for hospitals and health systems, now that the Centers for Medicare and Medicaid Services is tying a larger portion of reimbursements to Hospital Consumer Assessment of Healthcare Providers and Systems (HCAHPS) scores, the patient experience will now be a financial priority, too.

Medicare spending is projected to outpace GDP despite lower growth in Medicare Spend Per Beneficiary (MSPB), according to the Medicare Payment Advisory Commission (Medpac) June 2017 Report to Congress. MSPB fell to an annual increase rate of 1 percent for the period 2010 to 2015, but projections for 2016-2025 show a higher annual growth rate of 4 percent. By 2030, 81 million beneficiaries will be in the Medicare program and overall Medicare spending will increase 6 to 7 percent each year—a higher projection than the GDP, which is projected to increase 4 percent annually.

5) Hospital-acquired infections remain a persistent problem. Although progress is being made to prevent healthcare-associated infections (HAI), the Center for Disease Control (CDC) estimates one in 25 hospital patients acquires at least one HAI.

The physical environment is fourth on the list of HAI causes, according to the CDC. While HAIs from treatment-related causes are actually decreasing, HAIs resulting from the environment of care may not be. Hospitals must consider how they can improve the design, maintenance and management of facilities—from ventilation systems to room décor—to reduce infection risks.

"Aging infrastructure and the buildings themselves are beginning to fail patients and cause compliance problems, as providers continue to hold an 'it breaks, we fix it' mentality," said George Mills, Director of Technical Operations, JLL Healthcare Solutions. "At the same time, the aging workforce is resulting in a shortage of healthcare facility management (FM) staff. FM partners and young, tech-savvy talent have an opportunity to bring new skillsets and fresh thinking into the industry during its journey to population health."

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. Our vision is to reimagine the world of real estate, creating rewarding opportunities and amazing spaces where people can achieve their ambitions. In doing so, we will build a better tomorrow for our clients, our people and our communities. JLL is a Fortune 500 company with nearly 300 corporate offices, operations in over 80 countries and a global workforce of 83,500 as of March 31, 2018. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated.